Bad credit cost Aaron $65,000. But could it happen to you?

Here’s the ugly truth; having bad credit is one of the most costly financial mistakes you can make.

Things like homes, cars, and even student loans become exponentially more expensive when your credit score is less than ideal, and impossible to finance when you have bad credit.

Let’s use two people, Christina and Aaron, with two very different credit situations to show you what I mean.

Christina and Aaron have never met each other but they will soon. That’s because they are both about to buy homes in one of the hottest neighborhoods in the city. One right next to the other, each with the exact same layout and design.

The homes are brand new and, for the sake of argument, let’s assume they cost $250,000 each. The price is not negotiable.

Like most people, neither Aaron nor Christina has $250,000 in cash lying around so they each go to the bank and apply for a mortgage. Both plan to put down 20% ($50,000) and finance the remaining $200,000 over 30 years.

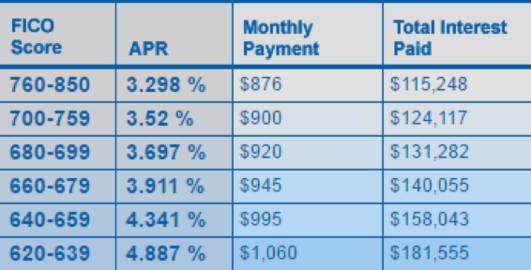

Christina is thrilled to learn that she has a credit score of 765, which is considered “excellent” by most lenders. Her high credit score allows her to qualify for an interest rate of 3.298%*, the best rate offered by the bank on any mortgage.

Aaron, on the other hand, has a much less pleasant trip to the bank. He fell behind on his credit card bills in college and missed a few payments here and there, causing his credit score to come in at 625. He is still approved for a mortgage, but at a higher rate of 4.887%.

On the surface, the difference between Aaron’s and Christina’s interest rates seems somewhat insignificant. But the numbers tell an entirely different story.

Introducing "How to Fix Your Credit: Do it Once. Do it Right. Get on with Your Life."

This step-by-step guide for motivated individuals who want to repair their credit once and for all includes:

- My simple, 4-step process to repairing and rebuilding your credit

- More than 20 actionable strategies and tips to dramatically increase your credit score

- Word-for-word scripts to take guess work out of credit repair. No need to reinvent the wheel here, my word-for-word scripts are ready to plug and play.

- The latest tools and tricks, as well as shortcuts, for improving your credit score with minimal time and effort

- Specific benchmarks to achieve at each step, so you know you’re on the right track

- The exact system I use to stay on top of my credit and personal finances with < 10 minutes of work each month. Why create your own? Steal mine!

- And more...

Plus: Lifetime access to any updates and revisions.

Comes with my no-questions asked, 30-day, 110% money back guarantee

Bryce knows the ins and outs of credit scoring and all the tricks in the book.

Bryce knows the ins and outs of credit scoring and all the tricks in the book. Many of which I had never heard of!

I can’t thank Bryce enough for showing me the way. I am looking forward to enjoying the ride without having to worry about my credit score on a daily basis.

- [1] Mortgage rates from www.bankrate.com

- [2] Median household income was $53,482 in 2014 according to the US Census Bureau

- [3] Average credit score from CreditSesame.com as of May 2016

I know this product is great, and I stand behind that. Which is why I am happy to offer a 30-day, 110% money back guarantee. Let me tell you why.

I spent YEARS building this product, distilling the best practices from my work with thousands of individual clients and sharing them in this one comprehensive book.

These methods have produced incredible results for people from a variety of different backgrounds, and I know they’ll work for you too.

So here’s my simple offer. If you don’t LOVE this product, I insist that you get your money back + 10% for your time. No questions asked.

That’s how confident I am that this product will work for you.

Buy now for only $47. Comes with my no-questions asked, 110% money back guarantee. We’ll talk about that in a minute.

I think that my eBook is the greatest credit repair product ever created. But of course I am biased, so I asked some of my readers to chime in.

Sample as of May 2016 1

Christina’s 3.298% interest rate comes to a monthly payment of $876 while Aaron’s 4.887% requires $1,060 per month.

Meaning that Aaron is paying $184 more than Christina, every single month, for what is essentially the exact same house.

Over the course of 30 years that $184 per month adds up to an extra $66,307 in interest.

That’s more than the average American household makes each year, completely flushed down the drain, all thanks to a three digit number called a credit score2.

$66,307 can be a bit difficult to comprehend on the surface so let’s break it down in to something a bit more relatable.

With Christina’s extra $66,307 she could:

- Buy a brand new Mercedes-Benz E-Class, complete with all the premium upgrades she likes

- Fly to Europe ~40 times, and still have money left over for sightseeing

- Buy 10,201 chicken burritos from Chipotle (which is one burrito per day for ~28 years)

All because she made the right moves regarding her credit.

And of course, this effect is not limited to just mortgages. Continuing with our example, Aaron will also be paying more than Christina for his student loans, car loan, credit cards, personal loans, and any other forms of debt that he may have.

Although fictional, Aaron’s situation is not uncommon for many people. In fact, his 625 credit score is actually that of the average American3.

So how do you make sure you don’t fall in to the same trap? Who can you trust to point you in the right direction?

I can help.

I’ve been researching credit and credit scoring since 2011. How to repair past mistakes….dramatically improve scores…prevent identity theft….and virtually every other area of credit you can imagine.

I started because:

1) I’m a geek for finance stuff.

2) I realized the INCREDIBLE importance that credit scores have on our financial well-being.

I knew that if I could improve my score even by a modest amount it would save me thousands of dollars in the long run. Dollars I could spend on traveling, savings, and just enjoying my life.

And most importantly, it would provide peace of mind in knowing that I will never have to deal with credit issues ever again.

So how can you do the same?

Well, you could pay one of the conventional credit repair companies to help you fix your credit. But that will cost you hundreds of dollars with no guarantee it will work.

Or you could do what thousands of other people have already done and use my proven system to fix the problem yourself, once and for all. So that you can get on with your life.

No more threatening phone calls from collectors.

No more drawer full of bills that you can’t bear to see.

No more living each day in fear.

Just straight-forward, actionable advice that is guaranteed to work.

Copyright © 2017 10xTravel.com